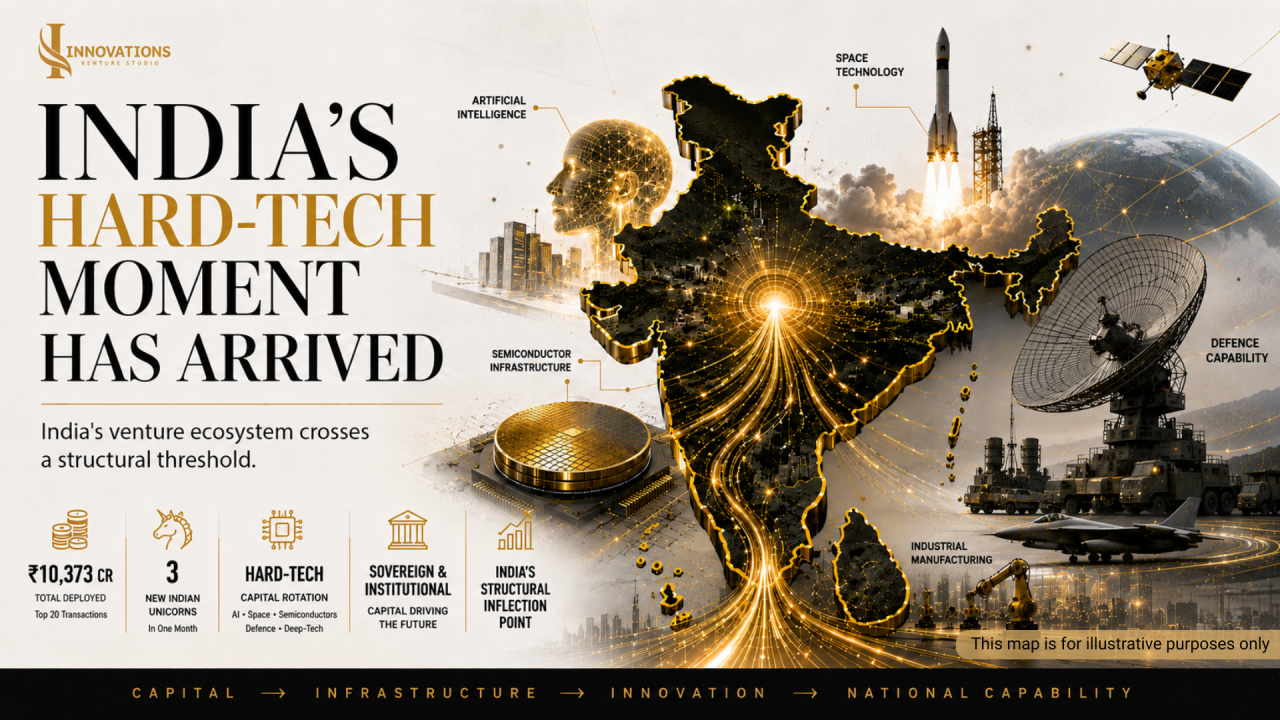

Three Unicorns. One Month.

₹10,373 Crore. The Market Has Started Voting With Capital

In a 30-day window between April 22 and May 21, 2026, twenty transactions totalling ₹10,373 Crore were tracked across India and global markets. Mobility led with India’s single largest round of the period. Food & Beverage returned as an institutional asset class. Aerospace and Defence attracted three deals in one month. And three Indian companies crossed the unicorn threshold in AI, fintech, and space. This issue decodes every transaction, derives every structural signal, and gives founders and investors a precise map of where conviction is concentrating.

Top 20 Deals Tracked This Period. Deep tech to consumer goods. Aerospace to fintech. Every round selected for strategic signal, not just size.

Where Capital Concentrated – By Industry

Mobility & Services Infrastructure leads capital deployed at ₹3,333 Cr across 4 deals, driven by Rapido’s ₹2302 Cr landmark round in ride aggregation. What matters more than the headline number is the composition beneath it: the remaining three transactions, Snabbit (home services marketplace), Aaritya (capital markets trading infrastructure), and Pronto (home services) are all operational infrastructure and services layer plays, not consumer applications. Capital is not chasing downloads. It is chasing density, repeat transactions, and network defensibility.

Food & Beverage at ₹1565 Cr across just 2 deals signals that India’s food manufacturing and packaged foods cycle is attracting serious PE capital patient, sector-specific, and supply-side in thesis.

Capital Goods spanning Aerospace & Defence and Electrical Equipment at ₹962 Cr across 3 deals is the structural breakout story of the period. Three transactions in a single 30-day window across Skyroot, Vem Technologies, and Kimbal Technologies is not coincidence. It is a coordinated capital signal that hard-asset, long-cycle industrial infrastructure has earned its place in institutional venture portfolios.

Not every deal is equal. These six transactions decode the deeper institutional logic behind the numbers.

01 · Rapido – ₹2302 Cr : India’s Mobility Platform Reaches Institutional Scale

Rapido’s ₹2,302 Crore round backed by Prosus (Naspers), WestBridge Capital, and Accel India is the period’s defining transaction. It validates the thesis that bike taxi and transit aggregation can command PE-scale capital when network effects are sufficiently entrenched. Rapido has built exactly that: a two-wheeler-first mobility platform with defensible unit economics in Tier 2 and 3 India, where four-wheeled taxi economics are structurally unviable. The Prosus participation among the largest global growth equity houses signals that the India mobility consolidation story is still in early innings relative to its eventual scale.

02 · Iscon Balaji Foods – ₹1445 Cr : The Invisible Infrastructure Play

A ₹1,445 Crore Series A in a processed and frozen foods company is the most structurally surprising deal of the period and the most instructive in thesis. Advent India PE’s conviction in Iscon Balaji reflects a long-horizon bet on India’s food manufacturing upgrade cycle: as cold chain logistics improve, organised retail deepens, and branded processed food penetration rises, scaled food manufacturers will command premium PE valuations. This is not a consumer internet play. It is an infrastructure-on-the-supply-side thesis with patient capital behind it.

03 · Skyroot Aerospace – ₹568 Cr : Space Tech Earns Sovereign-Grade Capital

BlackRock writing a cheque into an Indian space tech startup alongside GIC Singapore and the Shanghvi Family Office is the structural validation India’s space sector needed. Skyroot’s ₹568 Crore raise from this composition of institutional, sovereign, and UHNW capital demonstrates that hard-tech, long-cycle, deep-capex businesses can achieve institutional valuations in India when the market structure is right. The Iran crisis accelerated the geopolitical logic for space capability. Skyroot captured that capital re-rating.

04 · HRDWYR – ₹124 Cr : India’s Semiconductor Ambition Moves From Policy to Capital

HRDWYR’s ₹124 Crore Series A with Persistent Systems as a strategic co-investor is a milestone for India’s semiconductor ecosystem. It demonstrates a model the sector urgently needed: an anchor strategic investor providing not just capital, but a commercial integration and validation pathway. Persistent Systems’ participation creates an immediate customer relationship and product roadmap anchor. This is venture capital acting as industrial policy precisely the model that India’s chip ambitions require to move from aspiration to asset class.

05 · Aaritya Tech – ₹313 Cr : The Capital Markets Infrastructure Bet

Accel India and Elevation Capital co-leading a ₹313 Crore Series B in a trading platform is a vote of institutional confidence in India’s capital markets infrastructure layer. As demat accounts proliferate and retail investor participation deepens, the technology stack underlying trading, order management, and capital markets operations becomes a high-value, defensible infrastructure play. Two Tier 1 institutional investors co-leading is the strongest possible signal that this thesis has moved from narrative to conviction.

06 · LightFury Games – ₹103 Cr : When Athletes Become Institutional Capital

LightFury’s ₹103 Crore Pre-Series A backed by Mahendra Singh Dhoni, Jasprit Bumrah, Hardik Pandya, Shreyas Iyer, Ravindra Jadeja, Tilak Varma, Blume Ventures, Times Internet, and MIXI Global is the most structurally unusual transaction of the period. India’s top cricketers are not acting as celebrities endorsing a brand. They are acting as early-stage investors with structured equity positions. The Blume Ventures and Times Internet participation alongside them provides the institutional credibility layer. This is India’s gaming sector receiving a capital signal from both institutional funds and the most powerful personal brands in the country simultaneously.

What’s Moving the Capital

Geopolitical volatility as backdrop, India’s domestic capital architecture as stabiliser. How the investment environment looked in April–May 2026.

The Operating Environment

The fragile ceasefire brokered on April 8, 2026 has held. The Strait of Hormuz is partially reopened for non-US, non-Israeli vessels. Oil has stabilised but not normalised. The economic aftershocks from the Iran crisis are nowhere near fully priced in, and the institutional investment community knows it.

For India, the picture remains a study in resilience within constraint. Crude oil imports accounting for over 85% of India’s energy needs remain elevated in cost. The rupee has faced persistent depreciation pressure. Yet the equity market told a different story in April–May: the BSE Sensex recovered to pre-war levels, absorbed continued FPI selling, and held because domestic mutual fund flows, EPFO equity allocations, and SIP investors provided structural demand that simply didn’t exist in prior cycles.

This distinction matters enormously for founders and investors. India’s capital market resilience in a global crisis is not coincidence. It is the first-order consequence of a decade of retail investor onboarding, UPI penetration, and domestic mutual fund discipline. The same structural transformation that underpins India’s fintech story is now the shock absorber for India’s broader equity market.

IVS Macro Read: The geopolitical risk premium is now structurally embedded in the cost of capital. Founders who modelled capital availability on 2023–2024 parameters must re-anchor their fundraising timelines. The patient, domestic-led, conviction-first capital cycle is the new architecture not a temporary adjustment.

Three Forces Reshaping Deployment

Global LP caution persists – Endowments and sovereign wealth funds with Middle East exposure are maintaining reduced risk allocations to alternatives. For Indian founders raising international rounds, this means longer timelines, tighter terms, and harder conversations at LP closings.

Domestic Indian anchor capital stepped up decisively – The Rapido round, Skyroot raise, and Aaritya Series B – all India-anchored in institutional composition, show that domestic PE and VC capital is now capable of leading large rounds without requiring international co-investors as primary validators.

Strategic sectors are receiving geopolitical re-ratings – Defence, space, semiconductors, and clean energy are now commanding risk premia that were structurally unavailable just 18 months ago. Three aerospace and defence deals in a single 30-day window, Skyroot, Vem Technologies, and Dhruva Space is not coincidence. It is a coordinated signal from capital markets.

Five Signals Embedded in This Month’s Data

What the transactions reveal about the next 12–18 months of venture and private market activity in India.

- Geopolitics Has Created a Permanent Capital Re-Rating of Defence & Space

Aerospace and Defence received ₹7,533 Crore across three India transactions in a single 30-day window – Skyroot (₹568 Cr), Vem Technologies (₹185 Cr), and Dhruva Space (₹105 Cr via government fund). This is not a coincidence of timing. The Iran crisis structurally elevated the risk premium assigned to sovereign-grade capabilities in space, surveillance, dual-use technology, and satellite infrastructure. Founders in these verticals now have access to a funding environment combining private PE, sovereign wealth fund capital, and government innovation funds simultaneously that simply did not exist 24 months ago.

- Food & Beverage Resurfaces as a Serious PE Asset Class

Two Food & Beverage transactions totalling ₹1,565 Cr. in a single month is a structural signal, not a coincidence. Iscon Balaji (₹1445 Cr., Series A, Advent India PE) and Wingreens Farms (₹120 Cr, Series D, Ashish Kacholia + Alchemy) represent the two ends of the F&B capital spectrum: large-format PE and conviction-driven public market investor capital. The underlying thesis is India’s food manufacturing upgrade cycle, cold chain deepening, organised retail growth, and branded packaged food penetration rising in Tier 2/3 markets. F&B is no longer a consumer internet adjacency. It is a core PE infrastructure thesis.

- India’s Semiconductor Moment Needs a Business Model – HRDWYR Is a Template

HRDWYR’s ₹124 Cr Series A with Persistent Systems as strategic anchor investor is a template for how India’s semiconductor ecosystem can attract risk capital at scale. The traditional challenge for chip design startups is the absence of a domestic anchor customer without one, the commercial validation required to raise institutional capital is structurally unavailable. Persistent Systems’ equity co-investment solves this in one move: it simultaneously provides capital, de-risks the commercialisation path, and creates a reference customer for subsequent rounds. This model strategic corporates co-investing at Series A as validation anchors is the model India’s semiconductor sector should be replicating at scale.

- Services Marketplaces Are Consolidating – Capital Is Separating Winners From the Field

Three services marketplace transactions in one period Snabbit (₹529 Cr, Series D, home services), Pronto (₹189 Cr., Series B, home services), and Aaritya (₹313 Cr, Series B, trading platform) suggest that the marketplace infrastructure layer in India is entering a consolidation phase. Capital is concentrating in companies with network density, repeat transaction rates, and operational leverage. The Series D milestone for Snabbit backed by SIG, Mirae, and Bertelsmann signals that institutional crossover investors are now comfortable holding marketplace companies to late-stage. That is a critical milestone for the sector’s maturity.

- AI Capital Is Bifurcating – Foundational Infrastructure vs Consumer Applications

Two AI transactions with contrasting profiles: Sarvam (unicorn, foundational Indian language model) and M/Curious Digital (₹102 Cr Seed, AI-native personal assistant). The market is beginning to separate foundational AI infrastructure which requires long capital cycles and India-specific data advantages from AI application layer bets, which require distribution, UX, and fast iteration. Peak XV backing both Sarvam (at unicorn valuation) and M/Curious Digital (at Seed) is the clearest possible signal that one of India’s most sophisticated venture funds sees the full AI capital stack as a multi-year opportunity. Founders in both categories have institutional conviction available but the diligence lens, the capital quantum, and the timeline to returns are structurally different.

India’s Investment Inflection: Structural Conviction Meets Concentrated Risk

What We Are Building and Tracking

At IVS, we co-build companies. This section reflects our view formed by active engagement with founders, operators, and capital markets – not passive observation.

“The founders who build through the noise emerge with something capital cannot buy: a track record formed when conviction was genuinely scarce.” – Innovations Venture Studio.

₹10,373 Crore deployed across 20 tracked transactions in 30 days. Three unicorns. Two aerospace deals. One semiconductor breakthrough. A ₹1445 Cr. bet on frozen food. These are not isolated transactions – they are a pattern. And the pattern tells us that India’s venture ecosystem has moved, quietly but decisively, into a new structural phase.

The deep tech investment thesis – which required patient explanation to LPs as recently as 18 months ago now requires no advocacy. The capital has moved. What it still requires is the operational credibility to execute: regulatory navigation, talent pipeline construction, long-cycle product development, and financial discipline to manage extended runways. This is where venture studios, not passive investors, create asymmetric value.

On the capital environment: the cost of capital has structurally reset. Founders who anchored their Series A/B expectations on 2022–2024 comparable rounds are operating with a broken reference frame. The new architecture favours capital efficiency over growth at any cost, institutional-grade governance as a precondition for fundraising, and hybrid capital structures that optimise dilution without sacrificing growth. We are helping our portfolio companies navigate this in real time as active co-builders, not as strategic advisors.

FORWARD LOOKING LENS

What Modi’s Europe Tour Actually Signals

Five countries in six days. Nearly ₹3,34,000 Crore in investment commitments. Seventeen agreements with the Netherlands alone covering semiconductors, defence, AI, and green hydrogen. A Special Strategic Partnership locked in with Italy. The UAE putting ₹41,750 Crore on the table while West Asia still hasn’t fully stabilised. Strip away the protocol and the optics, and what you are really looking at is a government that has figured out how to use diplomatic bandwidth as an economic instrument. The sectors on every MoU signed across this tour energy security, critical minerals, deep tech, clean infrastructure are not chosen arbitrarily. They are the same sectors where India’s private capital markets are already moving, as this issue’s deal flow confirms. That alignment between what is being signed at the sovereign level and what is being funded at the venture and PE level is not a coincidence. It is coordinated industrial policy, even if no one calls it that.

The part that should matter most to founders and investors is subtler. Modi spent time with CEOs of some of the world’s most valuable companies firms that already have India exposure and are now being asked to deepen it. When a Dutch institutional investor or a Nordic sovereign fund sees its own government sign seventeen agreements with India, the conversation about India allocation inside that institution changes. Not because of the optics. Because the agreements reduce perceived regulatory and partnership risk and that directly affects LP committee decisions on India-focused fund commitments. The India-EU Free Trade Agreement, whose conclusion was referenced during the Italy leg, with a structured bilateral trade target with Italy alone by 2029, is the kind of structural unlock that takes eighteen months to show up in capital flows but shows up clearly when it does. The tour matters for founders not because of what was announced but because of what it makes easier to close, quietly, in the quarters ahead.

Anthropic Surpasses OpenAI: What a ₹80,000 Crore Round Signals

Anthropic closed a Series H at approximately ₹80,250 crore surpassing OpenAI to become the world’s most valuable private AI company. Led by Altimeter Capital, Dragoneer, Greenoaks, and Sequoia, the round raised ₹5,400 crore and nearly tripled Anthropic’s February 2026 valuation in a single financing event. The underlying driver is structural: Anthropic’s annualised revenue run rate has reached approximately ₹3,900 crore, powered largely by Claude Code, which has moved from productivity tool to enterprise-critical infrastructure. When a product embeds itself into daily knowledge work at this velocity, it stops competing on features and begins competing on switching costs, a distinction that separates durable AI businesses from cyclical ones. Foundation model companies are no longer being valued as technology ventures. They are being priced as emergent infrastructure monopolies. For Indian founders and investors, the question is no longer who wins the model race, it is which layer of the AI stack offers the most defensible position to build from.

Established in 1988, Pioneer Fabricators Ltd. is a specialised engineering and manufacturing company with a long-standing track record of serving India’s industrial and infrastructure sectors. Over nearly four decades, the company has built critical components including steel bridge girders for Indian Railways, locomotive chassis, turbine auxiliaries, pressure vessels, and other heavy engineering systems that form the backbone of national infrastructure.

At Innovations Venture Studio, we believe that India’s next phase of industrial growth will be driven by businesses that combine operational depth with institutional credibility. Pioneer Fabricators exemplifies this philosophy. Our engagement extends beyond capital to supporting long-term strategic growth, organisational strengthening, and institutional readiness.

As India accelerates investments in infrastructure, manufacturing, and industrial self-reliance, companies with proven engineering capabilities and execution discipline are positioned to play an increasingly important role in the nation’s development journey. Pioneer Fabricators represents the kind of enterprise that not only participates in this transformation but helps enable it.

Capital no longer separates India’s strongest companies from the rest. Execution does. The businesses attracting institutional conviction today share one foundation operational discipline, infrastructure relevance, and long-cycle durability. Not platform narratives. Not growth-at-any-cost. Structural importance to how India actually functions. That shift in what capital rewards is not temporary. It is the new architecture.

What stands out is not the scale of capital deployment, but where conviction is concentrating.

Institutional capital is increasingly backing operational depth over narrative momentum across AI, defence, manufacturing, energy, and fintech infrastructure. This is a structural shift.

Tighter capital markets are not weakening strong businesses; they are sharpening them. The next generation of enduring Indian companies will be built by founders who prioritise execution quality and capital discipline over velocity. The opportunity has not narrowed, it has become clearer.

Sources and References

CNBC | Tracxn Unicorn Club | PrivateCircle | The Tribune | India News Network | Outlook Business | Business Standard