The Reckoning Has Begun

India’s startup story in FY 2025–26 did not unfold the way the optimists scripted it and yet it was more consequential than they imagined. The year forced a long-overdue reckoning. Deal volumes contracted sharply. Valuations came under the scanner. The era of growth-at-any-cost is, finally, over. What replaced it is something more durable: a capital market that is learning to reward businesses with real fundamentals, genuine moats, and a credible path to profitability.

This is not a crisis. This is a correction and corrections, when digested well, are the preconditions for the next great wave of wealth creation.

At Innovations Venture Studio, we believe India is on the cusp of that wave. The infrastructure is laid. The regulatory environment is maturing. Global capital, having satiated itself on overpriced US AI bets, is looking East with renewed curiosity. The founders who built through the noise are now ready to run.

This inaugural edition of The Capital Dispatch maps the key transactions, structural shifts, and emerging opportunities that defined the fiscal year — and frames what FY 2026–27 must look like for those who intend to lead.

The Numbers That Defined The Year

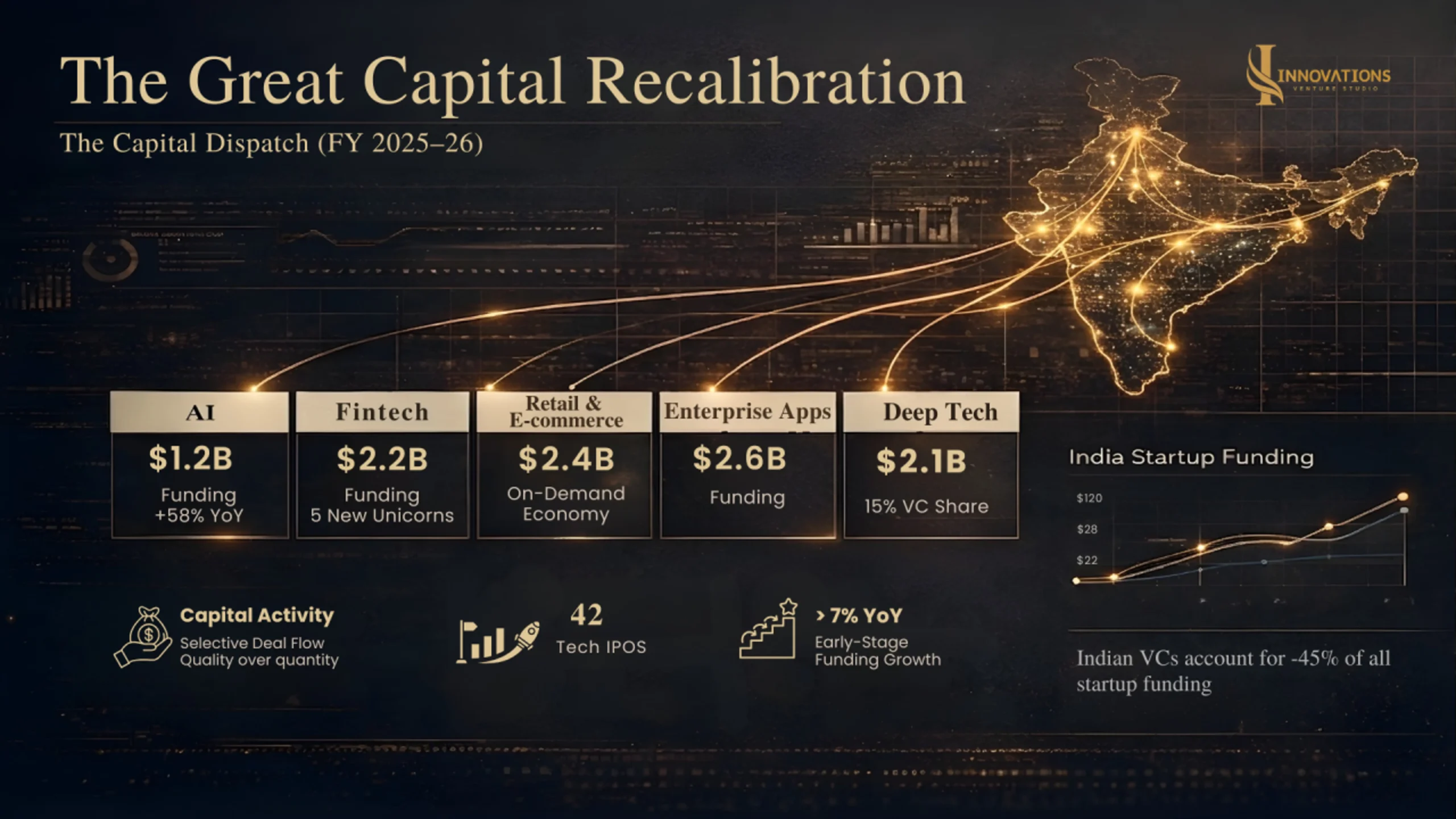

The headline numbers deserve context. A 17% decline in total funding sounds alarming in isolation. It is not. India’s tech ecosystem raised $10.5 billion in 2025 down from $12.7 billion in 2024, but still ranking third globally behind only the US and UK. The deals that did not get done in 2025 were, in most cases, the ones that should not have been done in 2022 either. The capital that did flow was more precise, more deliberate, and frankly, more sophisticated.

At the other end of the spectrum, public markets told a complementary story. India saw 146 IPOs collectively raise $7.2 billion in 2025, according to EY. The surge in listings reflects a market that is reopening selectively, rewarding companies with predictable cash flows, governance discipline, and credible paths to profitability.

Three structural realities define the FY25 landscape. First, late-stage capital contracted most severely down 26% to $5.5 billion as investors demanded proof, not promise, from companies approaching public markets. Second, early-stage funding showed surprising resilience, rising 7% year-on-year to $3.9 billion, suggesting that institutional conviction in the India story at the formation stage remains intact. Third, and perhaps most significantly, domestic funds stepped up. Indian VCs now account for nearly 45% of all startup funding, up from 28% in 2020 a structural shift that reduces the ecosystem’s vulnerability to global risk-off cycles.

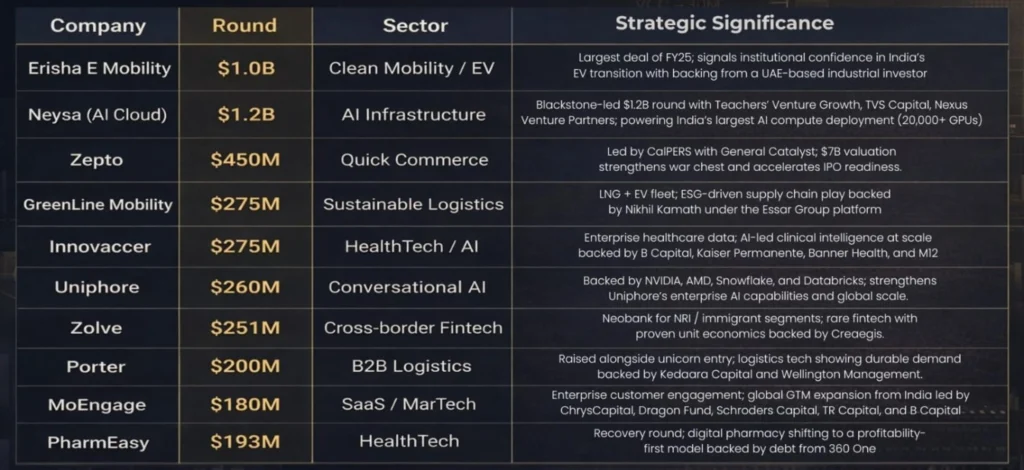

Deals That Moved The Needle

Below are the landmark funding rounds that shaped capital flow in FY 2025–26. They are not merely transactions — they are signals of where institutional conviction is concentrating.

Reading this table as a set of discrete events misses the point. Read it as a pattern and the signal is unmistakable: capital is concentrating in businesses with physical-world defensibility EV infrastructure, logistics, healthcare plumbing, and AI that sits on top of proprietary data. The era of pure-software moats built on marketing spend is over. The next decade belongs to companies that have built something operationally hard to replicate.

The IPO Year That Rewrote The Rulebook

If 2024 was the year India’s startup ecosystem asked whether public markets were ready for new-age companies, 2025 was the year it got its answer. Forty-two technology startups listed on Indian exchanges per Tracxn a 17% increase over 2024. Of these, 18 were new-age consumer tech startups that collectively raised ₹41,283.2 Cr crore, a record that dwarfs all prior years. For the first time in the ecosystem’s history, the IPO window became a genuine strategic alternative to late-stage private capital.

The Standout Listings

Urban Company debuted at a 58% premium. Meesho delivered a 53% first-day gain before settling into sustained outperformance. PhysicsWallah and Groww both validated the proposition that consumer-facing, unit-economics-positive businesses can command premium public market valuations. These were not flukes; they were the result of disciplined private-market journeys that prioritised real revenue over GMV fiction.

The Reverse Flip Phenomenon

Perhaps the most structurally significant trend of FY25 was the “reverse flip”: the mass homecoming of Indian unicorns from Singapore and Delaware back to Mumbai and Bengaluru. Razorpay, Meesho, and Flipkart completed their domicile shifts. Zepto, ShipRocket, and PhonePe are in the pipeline. The drivers are clear: SEBI’s progressive disclosure framework, a deep retail investor base, and the economic absurdity of paying double taxation in a foreign jurisdiction to access capital that ultimately reflects Indian consumer behaviour.

For India’s regulatory architecture, this is a validation moment. For founders sitting in Delaware holding companies built on India revenue, it is a strategic imperative. The question is no longer whether to flip back, it is how fast.

What 2026 Holds: The Pipeline IPOs

The 2026 IPO pipeline is, if anything, more consequential than 2025’s. Flipkart, PhonePe (already filed via SEBI’s confidential pre-filing route targeting a ₹12,000 crore issue), Zepto (confidential DRHP filed post Dec 2025 conversion to public limited company), Zetwerk, Moglix, and Cult.Fit are all expected to test public markets. If even half of these listings proceed at target valuations, they will collectively recycle billions in institutional capital back into the ecosystem creating the next vintage of angel cheques and fund commitments.

AI & Deep Tech: From Narrative to Asset Class

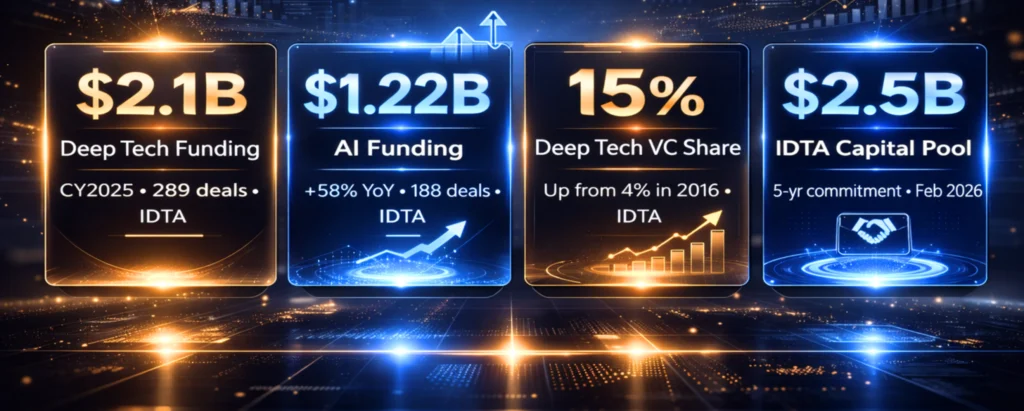

The most consequential structural shift in India’s venture landscape in 2025 is not captured by the funding headline. It is captured by a percentage: deep tech’s share of total VC-PE activity rose from 4% in 2016 to 15% in 2025. That is not a sector trend. That is a reallocation of the foundational investment thesis for an entire ecosystem.

The India Deep Tech Alliance’s inaugural 2026 report makes the case with precision: AI funding rose 58% year-on-year in 2025, crossing $1.22 billion across 188 deal ls. Non-AI deep tech — robotics, biotech, semiconductors, space — added another $1.19 billion across 147 deals. The Alliance’s dedicated $1 billion AI fund, to be deployed over three years within a broader $2.5 billion commitment with Nvidia and Qualcomm Ventures as technical anchors and $110 million already deployed into 50+ companies since September 2025), represents the first institutional-scale patient capital pool specifically designed for long-cycle deep tech development from India.

The Government as a Venture Capitalist

Perhaps the most underappreciated story of the year is the Indian government’s direct insertion into the venture stack. The ₹100 billion ($1.15 billion) state-backed Fund of Funds received cabinet approval in February 2026, but the policy groundwork laid across the year was equally significant. The startup classification window for deep tech companies was doubled to 20 years. Revenue thresholds for startup-specific tax benefits were tripled to ₹3 billion. The government co-led a $32 million round for quantum computing startup QpiAI, a rare and instructive signal of what ‘patient capital’ looks like at sovereign scale.

The critical insight here is not that the government is spending money. It is that government capital is beginning to price in externalities that private capital structurally cannot: national security, supply chain sovereignty, and decadal research cycles. For founders building in semiconductors, quantum, space, and biotech, this changes the risk calculus significantly. The addressable grant and equity pool just got substantially larger.

Where The Smart Money is Being Raised

Fund formation in FY25 told its own story. Over $12.1 billion in new fund corpus was committed across India-focused vehicles during the year, even as deployment remained cautious. The divergence healthy fundraising alongside selective deployment is a hallmark of a maturing LP base that is bullish on India’s long arc but disciplined about vintage risk.

Notable Fund Closes

- ChrysCapital X — ChrysCapital closed its tenth fund at $2.2 billion among India’s largest PE fund closes.

- Accel India Fund VIII — Accel raised its eighth India-focused fund at $650M to back category-defining startups across AI, consumer, fintech, and manufacturing, reinforcing conviction in India’s next generation of founders.

- Bessemer India Fund II — Bessemer Venture Partners closed its second India fund at $350 million, focused on AI-enabled services and SaaS.

- Peak XV Partners Fund I (post-separation) — Peak XV Partners raised a $1.3 billion independent fund the largest India-SEA venture vehicle post brand separation.

- Multiples Continuation Fund — Multiples Alternate closed a $430 million continuation fund, led by HarbourVest, Hamilton Lane, and LGT Capital Partners signaling evolving GP sophistication.

Where Capital Went – and Why It Matters?

Enterprise Applications: $2.6B

The largest single sector by capital deployed, enterprise applications held its position despite a 17% decline. The reason is structural: India’s SaaS export engine continues to generate dollar revenue at competitive margins, and global enterprises are increasingly comfortable with Bengaluru-domiciled engineering teams owning mission-critical software. The next frontier agentic AI embedded in enterprise workflows will accelerate this sector’s momentum through 2026.

Retail & E-commerce: $2.4B

The quick commerce revolution is the most operationally disruptive story of the year. Zepto, Blinkit, and Swiggy Instamart collectively reshaped consumer expectations around delivery timelines, forcing Amazon and Flipkart into expensive pivots. Flipkart’s “Minutes” service now operates across 800 dark stores. Amazon launched “Now (Tez)” targeting 300 micro-fulfilment centres. The market is projected to reach $35 billion by 2030. Meesho, notably, resisted the quick commerce pull and doubled down on value commerce for Tier 2-6 India, a contrarian bet that its IPO performance validated.

Fintech: $2.2B

India’s fintech sector demonstrated unusual resilience, recording only a 5% funding decline against a much sharper contraction elsewhere. The India Stack UPI, Aadhaar, Account Aggregator, ONDC continues to generate durable infrastructure moats that global fintech cannot easily replicate. Cross-border fintech (Zolve), embedded finance, and credit infrastructure for the underserved continue to attract capital. The projected $150–160 billion industry valuation by 2025-end reflects genuine economic activity, not paper marks.

Defence Tech: $311M in H1 2025

The most unlikely story of the fiscal year belongs to defence and space tech. Indian hardware startups historically starved of venture capital due to long development cycles and government procurement complexity raised $311 million in just the first half of 2025.

Raphe mPhibr’s mega round marked a first for the sector. Ten Indian spacetech companies, including Skyroot and Agnikul, were named Global Tech Pioneers by the World Economic Forum. The government’s PLI schemes and the opening of defence procurement to private players have finally unlocked venture risk appetite in a sector that should have been funded a decade ago.

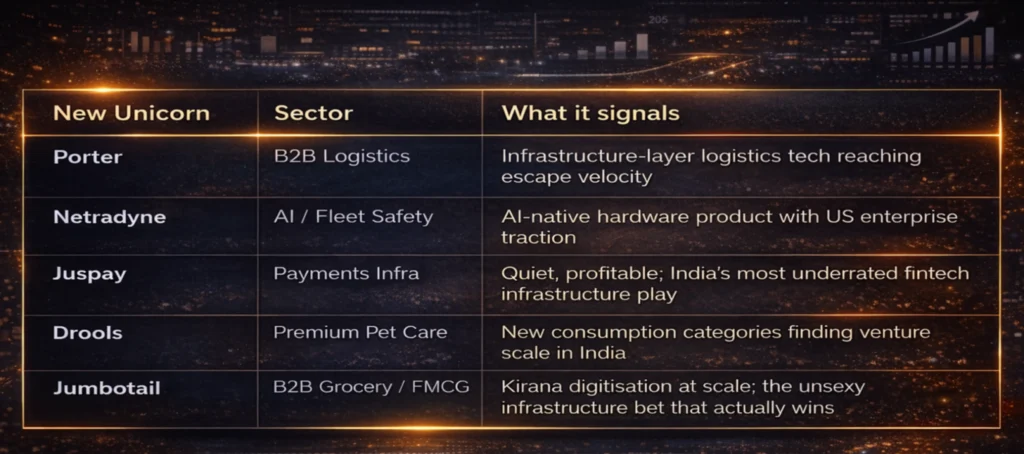

New Billion-Dollar Clubs

India added between six and eleven new unicorns in FY25, depending on the methodology applied. The cohort is instructive not for its scale but for its diversity. This is no longer a consumer internet club.

FY 2026-27: Five Theses That Will Define The Cycle

1. AI Infrastructure Beats AI Applications, For Now

Neysa’s $1.2 billion from Blackstone ($600 million equity, $600 million planned debt) signals that the institutional world has figured out something the VC world is still processing: In India’s AI journey, the compute layer is the first durable asset.

The deal announced at the India AI Impact Summit on February 16, 2026 is designed to deploy 20,000+ GPUs across India. GPU infrastructure, data annotation at scale, and model fine-tuning pipelines built for Indian language and behavioural contexts will attract infrastructure-grade capital lower return multiples, longer hold periods, but far more certain cash flows than application-layer bets.

2. The IPO Window Will Stay Open Longer Than You Think

With PhonePe, Flipkart, Zepto, Zetwerk, and Moglix all expected to test public markets in FY26, and investment bankers now treating ₹1.5–2 trillion annual mobilisation as the new normal, India’s IPO pipeline has structural depth. The retail investor base 15–20% of Indian households now invested in equities provides demand that did not exist five years ago. Expect 2026 to be the year that large global LPs begin benchmarking India public markets alongside private portfolios.

3. Deep Tech Will Separate the Serious Ecosystems from . the Followers

The IDTA’s $2.5 billion commitment, the government’s $1.15 billion Fund of Funds targeting deep tech, and Nvidia’s technical partnership with the Indian AI ecosystem are not independent events. They are coordinated infrastructure for a decade-long build. Founders in semiconductors, quantum computing, synthetic biology, and advanced manufacturing have a funding environment in 2026 that simply did not exist before. The window is open. The question is whether India’s talent pipeline can fill it.

4. Capital Recycling Will Fuel the Next Vintage

The IPO exits of 2025 — Elevation Capital’s ₹617 crore from Meesho and Urban Company at 36x and 19x respectively; Accel’s generational returns from Swiggy and Groww — are not just liquidity events. They are the upstream fuel for the 2026–28 angel and early-stage vintage. Successful founders become the next generation of angel investors and venture partners. That capital recycling flywheel is now spinning at meaningful RPM in Bengaluru, Mumbai, and increasingly, Delhi-NCR.

5. The Quality Filter Has Been Applied Permanently

Perhaps the most important structural legacy of FY25 is the discipline it has installed in the ecosystem. Boards are demanding cash flow visibility before Series B. LPs are scrutinising DPI, not just TVPI. Founders who built through the noise are now the ones raising — and they are raising at valuations that can actually deliver LP returns. This is not pessimism. This is what health looks like.

What We Are Building For

At Innovations Venture Studio, we occupy a deliberate position within this evolving ecosystem where capital, capability, and credibility converge to build the next generation of valuable Indian companies. We are builders, bridging capital with companies, ambition with discipline, and today’s ideas with tomorrow’s institutions. We work alongside founders at the point of maximum uncertainty, when conviction exists but the venture has yet to take shape, helping transform early belief into enduring enterprises.

The data from FY25 reinforces our founding thesis in three ways.

- Operational depth > capital access: Founders with strong fundamentals unit economics, product–market fit, and GTM strategy will win capital. We focus on building that operational muscle, not just funding pitch decks.

- Deep tech needs real partnership: This space demands patient, structured support from regulatory navigation to talent building and long-term product development. We act as co-builders, not just investors.

- Bridging the early-stage gap: India’s seed and pre-seed ecosystem remains undercapitalized. The biggest gap lies between idea validation and Series A readiness and that’s exactly where we operate.

As we enter FY 2026–27, our focus areas reflect the themes this newsletter has mapped: AI infrastructure and applied AI for enterprise workflows; deep tech startups requiring hands-on venture building rather than passive capital; D2C and brand-building plays with Bharat-scale potential; and cross-border fintech and SaaS with verifiable unit economics. We are actively partnering with founders, funds, and corporates who share the conviction that India’s next decade of wealth creation will be built by those who are willing to do the hard work now.

The Quiet Confidence of a Maturing Market

India’s startup ecosystem in FY 2025–26 did not produce a breakout AI lab or a global consumer platform. What it produced was something arguably more valuable: credibility. The IPO machine validated business models that were once questioned. The funding discipline weeded out noise. The government showed up as a structural partner rather than a regulatory friction. The domestic investor base deepened. And the next generation of founders many of them former operators from Meesho, Razorpay, Zepto, and Urban Company is now sitting on both the experience and, increasingly, the capital to build what comes next.

The window for building transformative companies in India has not closed. It has, if anything, clarified. The founders who understand that are the ones worth backing.

Sources And Data References

Tracxn | Inc42 | Indian Startup News | Autocar Professional | Blackstone | Neysa | TechCrunch | Business Standard | YourStory | The Hindu BusinessLine | Economic Times | PR Newswire | EE Times | India Deep Tech Alliance | Bloomberg | Accel | Bessemer Venture Partners | Peak XV Partners | Multiples Alternate Asset Management